The 3431 Savings Banks form the heart of the Group. Savings Banks are regional retail banks with total assets of about EUR 1.5 trillion. There is a local Savings Bank in every administrative region of Germany. Their activities focus on deposit and lending business with private and business customers (including the self-employed and local governments). With a network of more than 10,690 branches, Savings Banks are also the Group’s most important ‘sensor’ in the market. Typical business areas in which Savings Banks use the products and services of other Group members include payment transactions, securities business, international corporate banking and IT services.

Landesbanken provide a broad range of services for businesses and enterprises of all sizes. As central clearing banks for Savings Banks, the Landesbanken ensure the integration of Savings Banks into supraregional and international banking business. In addition, Landesbanken provide support and advice to the Savings Banks’ small and medium-sized customers in their international activities. In this way, the Landesbanken play a major role in developing new business opportunities for small and medium-sized enterprises. By bundling services, e.g. in international payment transactions and in the securities trading business, Landesbanken contribute to the cost efficiency of Savings Banks.

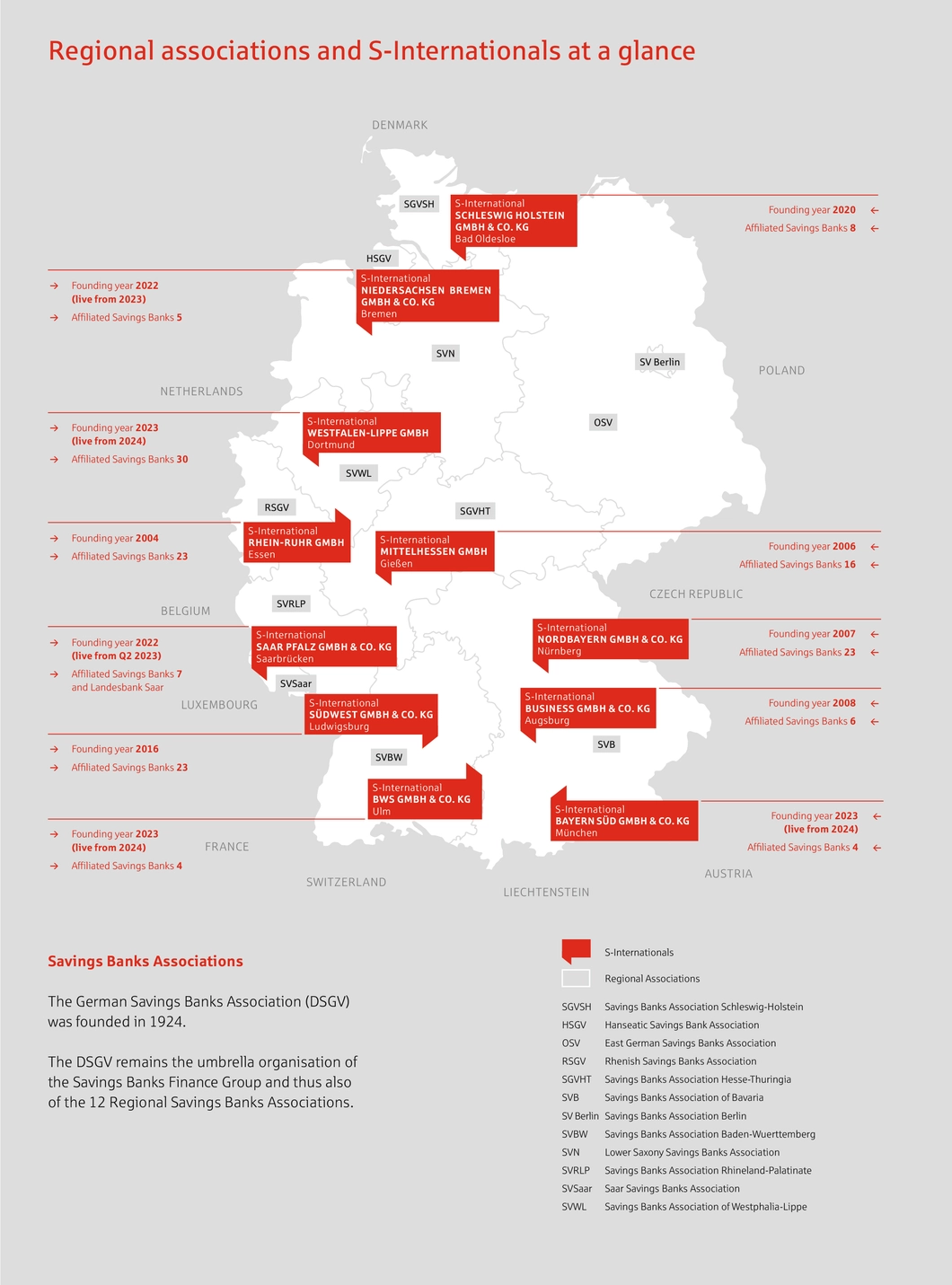

S-Internationals are the Savings Banks’ competence centres in which products and services relating to foreign commercial business are bundled for customers of cooperating Savings Banks. The first competence centre was founded in 2004 with S-International Rhein-Ruhr in Essen. 11 S-Internationals are now active throughout Germany. In principle they are run as independent subsidiaries of the participating Savings Banks

S-Internationals support companies in their international trade activities and foreign investments. The services offered by S-Internationals include foreign payment transactions, trade and export financing, documentary business as well as interest rate, foreign exchange and commodity management. Bundling the Savings Banks’ foreign business in S-Internationals has created a combination of qualified expert knowledge and high level of competence in international business.

1 As at 01 January 2025

The Deutsche Leasing Group is the solution-oriented asset finance partner for German small and medium-sized enterprises. The company provides support for investment projects in Germany and other countries and offers a wide range of financing solutions (asset finance) and supplementary services (asset services) for current and non-current assets. It helps its customers to finance change and innovation when it comes to the key transformative issues of our time – in the areas of decarbonisation, digitalisation and forward-looking infrastructure. Within the Savings Banks Finance Group, Deutsche Leasing is the centre of excellence for leasing, factoring and other alternative forms of financing. In its international business segment, Deutsche Leasing supports its German customers’ activities in more than 20 countries. For over 60 years, Deutsche Leasing has helped its small and medium-sized customers from industry, commerce, and both the service and public sectors to invest in innovation and transformation.

DekaBank is the Savings Banks’ securities service provider and, together with its subsidiaries, it forms the Deka Group. With assets1 under management totalling EUR 381 billion and around 5.5 million managed securities accounts2, the Deka Group is one of Germany’s largest securities service providers. It provides private and institutional investors with access to a wide range of investment products and services. DekaBank is firmly anchored in the Savings Banks Finance Group, and its portfolio of products and services is entirely tailored to the requirements of its owners and its sales partners in the securities trading business.

The five Landesbausparkassen (Savings Banks’ building societies) are the market leaders in Germany with a market share of 33.2% in terms of the number of new home loan and savings contracts and 35.7% in terms of the contract portfolio (number of contracts). They have 503 advisory centres and employ 6,285 office and field staff. At EUR 76.4 billion, the LBS Group’s cumulative total assets reached a new high at the end of 2023.

The eight public primary insurer groups generated gross premium income of EUR 22.3 billion in 2023, thus confirming its position as the secondlargest insurance group in Germany. The Regional Savings Banks Associations are the main sponsors or owners of almost all of the public insurers.

companies6

5002

2,919employees

8

3435

Savings Banks

5

(LBBW, BayernLB, Helaba, NORD/LB, SaarLB) + LB Berlin/Berliner Sparkasse

1493

This corresponds to a share of 43% of the 343 Savings Banks, and the trend is rising

Deutsche Girozentrale2

5,492

employees

5

1 Total assets include mutual and special funds, ETFs and certificates

2 As of 31 December 2023

3 As of 31 December 2024

4 As of 30 September 2023

5 As of 01 January 2025

6 Including associations and other institutions; figures have been rounded

7 Business volume here = balance sheet total/portfolio volume/ total assets/investment volume; figures have been rounded

8 Including foreign branches as well as domestic and foreign subsidiaries of Landesbanken

9 Excluding foreign branches, excluding domestic and foreign subsidiaries of Landesbanken

10 Offices/information centres

11 Office staff and field force, excluding part-time employees; figures have been rounded

12 Including 3,503 employees of associations, their institutions and other institutions

The Savings Banks Finance Group is a reliable partner for businesses and banks worldwide. International support for corporate customers is provided through the Group's international network.

While their focus on small-scale financing and services ensures moderate risks and stable earnings, Savings Banks also benefit from cooperating within the Group and with the Landesbanken. Division of labour increases operational efficiency in areas such as back office and IT services or the joint use of risk assessment models.

Members of the Group share the mutual trademarks and 'Sparkasse'. And in the event of economic difficulties, Savings Banks assist each other at regional or supra-regional level to ensure the continued existence of an institution through the Group's Institutional Protection Scheme.

For over 200 years, the Savings Banks’ concept has combined banking business with a sense of civic responsibility. Since its inception, the Savings Banks’ business model has focused on the region in which the Savings Bank is based, promoting the common good in its home region. The decentralised structure of the Savings Banks Finance Group ensures the local provision of carefully tailored risk assessment and customer solutions.

First Savings Bank in Hamburg was founded

The idea of Savings Banks has strong roots in Germany. Savings Banks can look back on two centuries of active involvement in regional development and of financial success in a highly competitive environment. The foundation of the Savings Banks’ business model lies in the 18th century proposition that everyone should have a fair chance to improve their lives through savings and retirement provision.

Savings Banks spread across the country in the 19th century and played a decisive role in financing the industrialisation of Germany.

At a time when there were still no comprehensive social security systems, Savings Banks were key in providing financial services to low-income households in particular, even in small communities.

Introduction of the giro system

The introduction of giro transactions is an important historical milestone. It marks the beginning of the development of the Savings Banks into modern credit institutions. At the same time, it is the starting point for the emergence of the network between Savings Banks and Landesbanken.

Savings Banks become legally and economically independent

Savings Banks contribute to the reconstruction of Germany

As it was in keeping with Germany’s federal structure, the model of decentralised Savings Banks – supported by local authorities or municipalities – quickly set a precedent.

Originally, Savings Banks were primarily active in the savings business, but they have operated as full-service retail banks since the beginning of the 20th century. Their responsible approach to banking and their local focus remain unchanged.

The introduction of cashless payment transactions in 1909 marked the beginning of the Savings Banks’ cooperation with the Landesbanken. Over the years, the Savings Banks Finance Group has been complemented by additional specialised service providers, for example in asset management, insurance etc.

The first Landesbanken were established in the mid-19th century in various parts of Germany.

They developed into central banks for the Savings Banks of a given region and soon became an important provider of local government finance. Today, Landesbanken operate both in Germany and abroad. They are predominantly active in wholesale banking. However, Landesbanken have retained their regional roots and operate as service providers for Savings Banks, for example, in more complex product areas.

Savings Banks support German reunification

The German regulatory regime applies equally to all banks, including Savings Banks. However, the legal framework and business model of the Savings Banks have a number of special features, many of them a legacy from their founding days and a tribute to Germany’s diversified economic structure.

Savings Banks were established to provide all citizens, including those on low incomes, with the opportunity to deposit their savings safely. This founding mission has evolved over time and was enshrined in law as a so-called public mandate, including the obligation among other things:

Therefore, Savings Banks are oriented toward the common good. Their business model is not aimed at generating maximum profits, but to fulfil their public mandate on a permanent basis. Moreover, the profits generated by the Savings Banks benefits – insofar as they are not required to strengthen equity – only the general public.

The public mandate shapes the Savings Banks’ business model and entrusts them with an economic and social responsibility that goes far beyond banking services.

Initially, Savings Banks were founded by citizens; their structure was reminiscent of private foundations. Later, they were founded predominantly by municipalities and integrated into the local government organisations. This legal structure was replaced in 1931, when Savings Banks became legally independent institutions. Since then, Savings Banks have operated under market conditions as legally and economically independent institutions under public law.

As opposed to other countries, Savings Banks in Germany have neither owners nor members. Instead, they operate under "municipal trusteeship". Their "responsible public bodies" are the municipalities.

However, as the municipalities are not owners or shareholders of Savings Banks, they cannot be sold by the municipalities. In short, Savings Banks are not state-owned banks. They are fully independent in their day-to-day business and run by licensed bankers.

Unlike Savings Banks, Landesbanken are owned primarily by Germany’s federal states and by the Savings Banks based in their respective federal state.

Savings Banks only service a clearly defined business area, which is specified as the administrative region of the municipality or district in which it was founded. The regional principle is enshrined in law. By focusing on their territory, Savings Banks operate very close to the market, balance risks carefully and take a long-term approach with their clients and the community as a whole. Their clear local focus helps Savings Banks to fine-tune products and services to meet local needs. This depth of knowledge, rarely found in remote corporate headquarters, contributes to the Savings Banks’ efficiency.